A Venture Capitalist Walks into a Prison…

The average non-minority American has probably heard of the “prison crisis”, or maybe even watched a documentary or two that made them fleetingly sad for a 60-90 minute stretch. But how big is the prison problem anyway? If a fledgling venture capitalist took some time between his B2B SaaS diligences to look at the prison market, what would he find?

1) The market is massive.

Sociologists at the University of Georgia released groundbreaking research in 2017, finding that 8.11% of the overall U.S. population has a felony charge. That’s just over 1 in 12 individuals—or ~26 million people.

A Wall Street Journal piece in 2014 adds equally staggering figures to show the full breadth of this workforce dislocation:

Over the past 20 years, authorities have made more than a quarter of a billion arrests, the Federal Bureau of Investigation estimates. As a result, the FBI currently has 77.7 million individuals on file in its master criminal database—or nearly one out of every three American adults. Between 10,000 and 12,000 new names are added each day.

One-third of individuals face challenges navigating the workforce for a singular mistake they made in their lives. One in twelve has a particularly difficult time re-entering due to the more punitive criminal measure of a felony charge. If those statistics don’t resonate, in 2015 the Brennan Center for Justice found that as many Americans have Criminal records as college diplomas. Bottom line—the market is astoundingly large.

2) The market is disproportionately minority and male.

8% of individuals in the U.S. have a felony charge, but 33% of black males have a felony conviction. This 33% figure again derives from the supremely well-researched longitudinal study, The Growth, Scope, and Spatial Distribution of People With Felony Records in the United States, 1948–2010, revealing the direct link between the War on Drugs farce and the precipitous rise of black male felony rates from 13% to 33% between 1980 and 2010. It is as if our collective incarceration policies were designed to compete with 1780-1810 for the worst 30-year period to be a black man in this country.

We should be further reminded that this 33% figure is for felony charges, implying that the percentage of black Americans with any criminal record (non-felonies included) is even larger. While it is hard to track down a precise national figure on this, we do know that nearly half of all black men (49%), 44% of Hispanic men, and 38% of white men are arrested at least once by the time they’re 23. These arrest rates are appalling across racial lines, though the racially-based delta remains persistent. Compounded by the fact that, on average, black men who commit crimes receive federal prison sentences that are 20% longer than white men, we can begin to understand why prison populations have evolved into heavily minority-majority populations. The statistical evidence is overwhelming here; these are just a few waves in the tide.

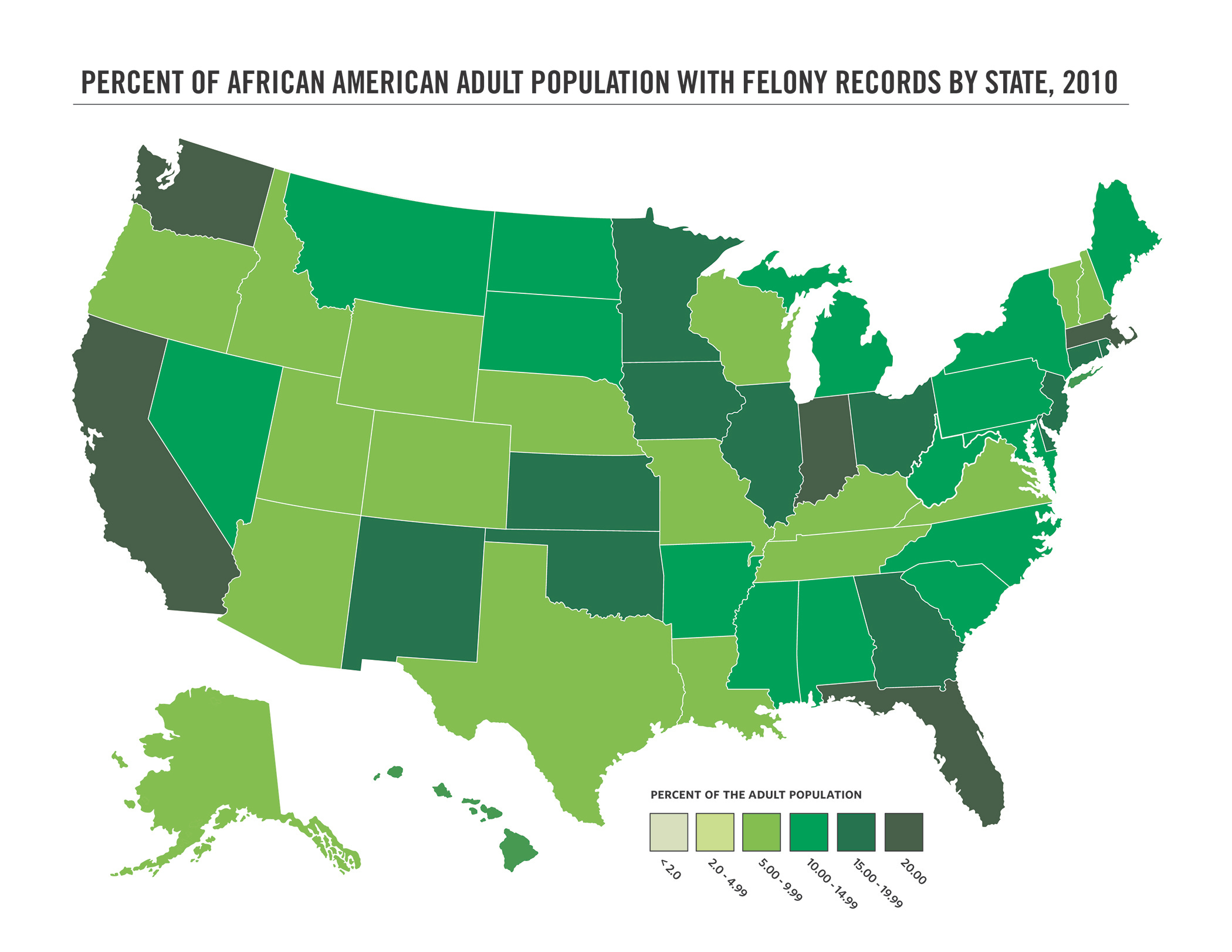

One last point is easier to grasp when visualized. The population of all African Americans with a felony charge (women included, hence the slightly more charitable-looking figures), shows states like California and Washington right alongside Florida, Georgia, Michigan and Illinois. Though racial discrimination certainly has its deepest, most vocal roots in the Southern United States, mass incarceration is by no means bound to just one political party.

3) The market is ripe for disruption

Yes, there is bureaucracy and legacy. The prison system is one of the towering physical artifacts of Jim Crow—slavery and sharecropping in unapologetic concrete. But out of great evil comes great opportunity.

Employers in every state want individuals who can get the job done, from low-skilled labor to the highest rungs on the corporate ladder. Oftentimes, criminal records indicate a mistake made by an individual, but typically have no bearing on whether they can perform a particular job. Employers know it—and applicants know it.

This labor market disconnect has been relentlessly stubborn, and a number of attempts continue to be made. Workforce development organizations, city/state partnerships with employers and Work Opportunity Tax Credits (WOTCs) are all stabs in the right direction—but they typically fail to address the following:

Employers need to go beyond issuing blanket hiring policies, such as “we don’t hire felons or ex-cons”, without any acknowledgment for the spectrum of severity or type of criminal charge. All crimes are not created equal—and the ease with which individuals safely re-enter the workforce should be at least remotely proportional and/or related to the charge on each individual’s criminal record.

People with convictions of all stripes need to have an idea of which employers will actually hire them. Going through the process of an application, multiple interviews, seemingly one step away from a “yes”—only to get dinged during an automated background check is a waste of everyone’s time. Policies need to be clear and readily accessible for all parties. To neglect this is to create major labor market friction and consistently wasted effort.

Employers need a way to reach eligible candidates and view their credentials and criminal histories objectively. If an employer doesn’t care about hiring individuals with a given offense on their record, how can they find and filter for these job seekers? Haphazard datasets from parole officers or state prison systems don’t count. It should be clear where those who were formerly convicted can be reached and fairly assessed to fill employers’ own workforce gaps.

Perception changes with re-conception

In short, a venture capitalist has plenty of reasons to get excited about a market like this. Platforms connecting employers to formerly convicted members of society eager to rejoin the workforce are a must, and investors should keep their eyes peeled for companies successfully putting these types of offerings together. But the average venture capitalist is also a pretty confident sapien, self-assured they know a decent amount about most worlds they encounter.

So VCs can succumb to the same human pitfalls in perception as the rest of us, which is especially important for this industry. At bottom, unlocking this workforce market requires unpacking long-cemented stigma—an inability for investors, politicians, employers and much of the general public to (a) forgive, (b) think beyond labels like “convict” and (c) re-evaluate individuals based on merit.

If someone went to prison for the all-too-common offense of possessing a small amount of marijuana in the wrong state, is it realistic to assume away their capacity to hold any and all jobs under the sun? Particularly if he or she was holding down a job and supporting a family when they were initially convicted, why should the tacit assumption be that all job-related skills instantly dissolve upon receipt of a criminal charge, no matter how small? Of course, if a crime is directly related to the job description—a bank teller and a charge of embezzlement—an employer ought to have some recourse to know this information. But for the vast majority of individuals who committed a minor offense—and for a large fraction of those who committed felonies as well—with the right training and skills, they should still be given the opportunity to perform a wide array of jobs they’re capable of performing. This last sentence is normative in nature, but the more important point is not. Our current treatment of those with criminal records reveals our default assumption to be that economic dislocation is deserved.

A second chance is the most basic premise for our country’s existence — immigrants fleeing to our country for a life that was better than what they had before. We need to offer second chances and get to work designing mechanisms to facilitate those chances. The reward will be one of the greatest economic uplifts in the history of American society, a powerful tailwind to reducing inequality, and a systemic force finally punching in the weight class needed for modern racial justice.